On a night in March 2020, two hundred tablets sat on the courtside seats of an arena in Atlanta, one on every seat, and they worked. Rafael Nadal was on the court. The tablets were ours — Alfi's — running live, recommending, responding, doing the thing we had spent four years and a family fortune building them to do. I stood in that arena and watched strangers pick them up and use them, and I let myself believe we had made it.

Eighteen months later, armed guards walked into our offices while a board meeting was still going on, and the company I built was taken from me. Within a year it was in bankruptcy, its patents transferred to the man who had engineered the removal, and fourteen thousand shareholders had nothing. And of everyone in that story, the person the United States government chose to pursue was me.

I am not writing this to litigate anything. I settled with the Securities and Exchange Commission, and I am not re-opening that here. I am writing it because the record of what actually happened to Alfi exists — in emails produced in discovery, in board recordings, in a resigning director's letter, in the company's own filings, in the patent office's public database — and almost no one has seen it. I think, when you see it, you will have the same question I do.

What we built

Alfi began with my son. Charles is an artificial-intelligence engineer, and where I saw the dumb advertising screens that had colonized every elevator and gas station, he saw a problem worth solving — and a principle worth holding. Make the screens intelligent, he said, but recognize what, not who: no cookies, no stored faces, nothing that ever leaves the device. In an industry built on tracking people across the internet, we set out to build the one platform that refused to.

It was not a pitch deck. A patent issued — U.S. Patent No. 10,784,696 — with Charles named as a co-inventor and the prosecution handled by Knobbe Martens, one of the top intellectual-property firms in the country. We built an engineering organization of some forty people in Belfast, chosen because Northern Ireland has a deep, underpriced pool of talent out of Queen's University, and they built a working computer-vision platform. On the company's own internal benchmark, our facial model edged Amazon's world-class Rekognition service.

And Alfi looked like something — because my wife Rachael made it so. She was there from the very first day, and she built the company's identity: its name and logo, its brand, and the voice of everything it said to the world. Charles made the technology work; Rachael made it something a stranger would trust enough to pick up. The tablet that drew that arena in was his engineering and her design.

And we deployed it — which, in a field full of vaporware, is the part that matters. Alfi tablets ran live in Belfast's Value Cabs taxi fleet, wired into the cars by uniformed technicians and photographed doing it. They ran at Belfast International Airport, in a London shopping centre, in an American Eagle storefront, and across a professional installation operation for rideshare drivers in Miami. In a measured one-week trial at the Culloden Estate outside Belfast, thirty tablets logged 324 users and roughly 4.4 million interactions, with click-through rates several times the industry standard.

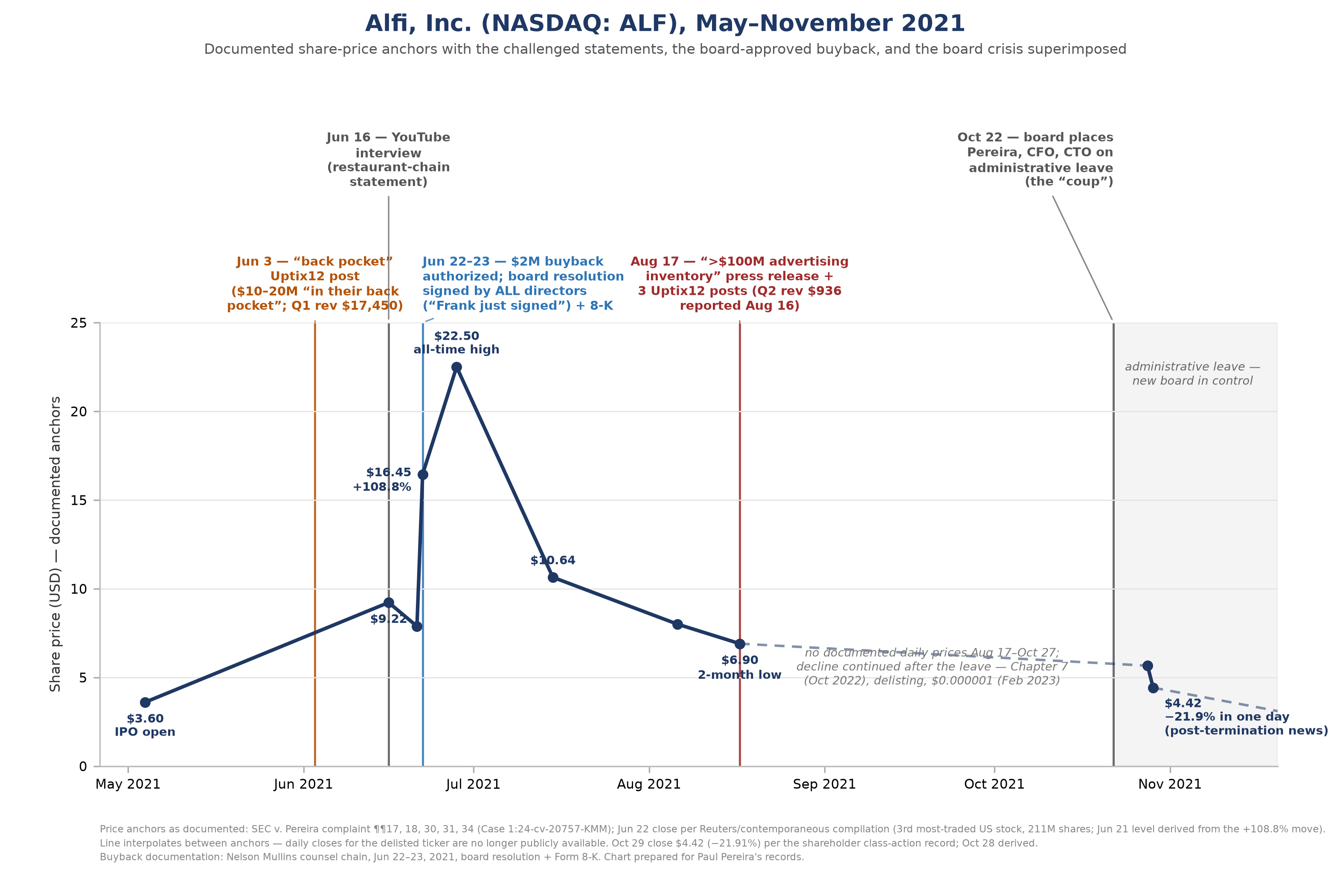

In May 2021 we took Alfi public on the NASDAQ, under the ticker ALF, led by Kingswood Capital Markets. For a family that had put five years and millions of its own money into an idea, it was vindication — our shares changing hands on the same exchange as Apple's. Within weeks the stock became a national retail-trading phenomenon; I went on Fox Business, live, "pleasantly surprised." And I want to be precise about something, because it matters later: I never sold a single share. A lock-up barred it. I made no money taking Alfi public. I put my own money in.

There is one more thing the record shows about how I ran the company, because it cuts against the story that was later told about me. The business decisions that would be questioned were not made by me alone in a room. They went through the company's officers and its lawyers. The consulting agreement with a restaurant founder was drafted by our CFO and routed, in his words, for "a review by Ken" — our corporate counsel. The stock buyback was run by our securities counsel at Nelson Mullins for regulatory compliance and signed by every director. The sponsorship agreement's final version was prepared by corporate counsel. These are not the fingerprints of a man freelancing; they are the ordinary paper trail of a company run through professionals.

The turn

The man who would take it was on my own board. Through his company, Lee Aerospace, Jim Lee was Alfi's lender and its largest shareholder, and his companies had held a security interest over Alfi's intellectual property since early 2020. He wanted the IP. I want to be careful here and stay with the record — so I will let the record speak.

On October 22, 2021, a special board meeting removed the founders — me as CEO, Charles as CTO, and our CFO. It was not, on the record, a deliberation. The one independent director who might have objected, the chair of the audit committee, was kept out of the planning. No charge sheet, no resolution, and no written warning was circulated. Armed guards entered the WeWork offices before the meeting had even adjourned, and the staff, frightened, left. Our corporate counsel warned that it was rushed and could "damage the company and destroy the stock value." He was overruled.

When counsel asked the one question that should have had a careful answer — why the CTO, the man who had built the technology, was being removed — the answer, as recorded in my contemporaneous letter to counsel, was immediate:

Well because he controls the companies IP.— attributed to Jim Lee, October 22, 2021 board meeting

Not fraud. Not mismanagement. The intellectual property. Days later, the one truly independent director resigned. His letter is, to me, the plainest verdict in the whole affair, and I quote it exactly because I want you to weigh his words, not mine:

The decision to replace the CEO/Founder, the CFO and the CTO in my opinion was personal and calculated and driven by certain directors/shareholders to take control of the company without any regard for due process… made through clandestine meeting… It was clearly fait a compli. Particularly concerning is the fact that there was already a mobilization for the removal of these officers by handpicked replacements whilst the meeting was still taking place.— Richard Mowser, independent director and audit-committee chair, resignation letter, October 26, 2021

An independent director does not resign in those terms over a legitimate investigation.

The unraveling

What followed proved which side could actually run a company. The new board's own conduct is documented in the company's own filings, so none of this rests on my characterization.

First, they lost the auditor — by concealment. When the audit-committee chair resigned, the reconstituted board did not tell the company's outside auditors. Days later the auditors resigned. A board that had seized the company in the name of good governance lost it its accountants within a week, by hiding a director's departure from the very people whose job was to know.

Then they rushed a new Chief Technology Officer into place over my recorded objection — a man who had been at the company three weeks, whose premature title triggered a six-figure liability and short-circuited a working succession plan. It was under that hastily installed CTO that the platform Charles built went dark for months, spanning the Super Bowl — an outage the new board never disclosed to shareholders. The interim chief executive they installed, Peter Bordes, presided over the loss of the auditor, the missed filings, and the slide toward delisting, and was ultimately removed.

You do not have to take my word for the wreckage. The company's own Form 8-K in March 2022 — signed by the new leadership, months after we were gone — conceded that its prior financial statements "should no longer be relied upon," that material weaknesses existed in its internal controls, that its quarterly report was delinquent, and that it had "very limited cash on hand." Every one of those admissions describes their tenure. When I left, there had been roughly twelve million dollars in the bank.

Then came the end, and it executed the motive stated in the boardroom. Jim Lee re-encumbered the company's assets, made himself interim CEO — becoming, at once, the lender, the controlling director, and the chief executive of his own debtor — and, the records indicate, caused the company to pay sums to insiders in the weeks before he put it into Chapter 7. Then, rather than restructure a company he had called "a billion-dollar company," he filed it into liquidation on October 14, 2022 — and moved, four days later, to have the intellectual property abandoned directly to Lee Aerospace. Through a credit bid — offsetting his own debt instead of paying cash — the technology changed hands.

That last fact is not my allegation; it is a public record you can check. The United States Patent and Trademark Office's assignment database today lists the owner of Patent No. 10,784,696 — the invention that still carries my son's name as a co-inventor — as Lee Aerospace, Inc. and Lee Digital LLC, reassigned to them in 2023. Fourteen thousand shareholders received nothing. The people who invented Alfi, branded it, built it, and took it public got nothing. On the documents, this was not a business that failed. It was an asset strip, carried out by the one man who occupied every role that might have stopped it.

My son

Charles was the co-founder, the CTO, and a named inventor on the patent — the person who actually built the thing. He was placed on "administrative leave" with the rest of us and terminated six days later, the stated reason a technicality about a Google account. His lawyer named it for what it was, in a letter at the time:

The "administrative leave" … is not an administrative leave at all, but rather is termination without Cause.— Constance Oberle Geoghan, Esq., counsel to Charles Pereira, October 28, 2021

He did not accept it quietly. As his contract required, he took his claim to arbitration — a real, filed case. But the same bankruptcy that stripped the company also shielded it: the automatic stay froze his arbitration, and the American Arbitration Association has confirmed it "remains in abeyance," unable to move until the bankruptcy court permits it. That bankruptcy is still open. So my son's claim against the company he built sits frozen — filed, real, and waiting — behind the wall the liquidation raised.

When the government came

Three weeks after we were marched out, the SEC opened an investigation, and in February 2024 it sued me over three statements I made in the summer of 2021, in the middle of a stock that had gone vertical. I resolved that matter on a no-admit, no-deny basis. I am not disputing that resolution on this page, and nothing here should be read as doing so. What I want to lay beside it are facts that are simply a matter of record.

The staff assembled an enormous file — our emails, my sworn testimony, tens of thousands of documents — more than a year before it filed. That file, produced under the confidentiality legends that mark material given to the Commission, was as complete as it would ever be long before the case was brought. The complaint sought no disgorgement — because the lock-up had barred me from selling a share, and there was nothing to disgorge. I profited nothing. And there is a cruelty in the timing that still stops me: the same October 2021 removal that put me on leave had cut off my access to my own company email — the account where much of that record lived — so for much of this I could not even read back my own words.

I do not ask you to conclude that I said nothing loose or too optimistic in the noise of a rocketing stock; a founder live on a soaring ticker is not a careful man. I ask the narrower, fairer question the documents raise on their own — the question of who was held to account. The government pursued me, alone, to a permanent bar and a penalty I cannot pay. The men who planned the removal in the dark, seized the company, lost its auditor, let its platform go dark, paid themselves on the way out, and walked away owning its patents — were charged with nothing at all.

Why I am telling this

I lost the company, the savings, the home. I am past the point where telling this changes my circumstances much. But fourteen thousand people put their money into what we built, and they were wiped out by a process that, on the documents, looks nothing like the story the public was given. My son's name is still on a patent that now belongs to the man who took it. And the record that shows all of this — every email, every recording, the resignation letter, the filings, the patent assignment — has been sitting in a discovery production almost no one has read.

So I have gathered it, and I am putting it where it can be seen. I am not asking anyone to take my word for any of it. I am asking you to read the record, and to ask the question it asks: how does this happen, and why was the founder the only one who answered for it?